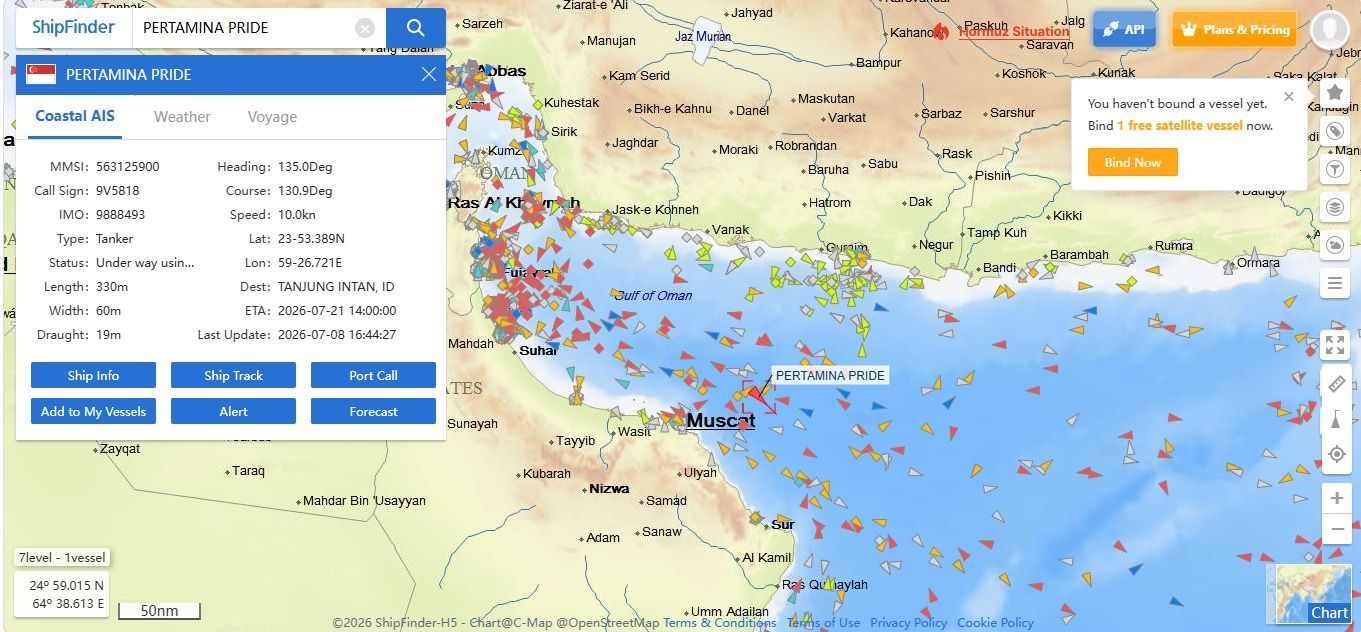

Global oil markets have entered another period of heightened uncertainty, despite earlier signs that prices were beginning to ease during the latter half of 2026. Expectations of rising production and a gradual shift toward an oversupplied market have been undermined by the renewed escalation of tensions between the United States and Iran in early July. As a result, the Strait of Hormuz—a critical maritime corridor that handles nearly one-quarter of the world’s oil trade and serves as the primary export route for Persian Gulf producers—has once again become a focal point. Given its strategic importance, even limited disruptions in the strait could quickly send shock waves through global markets and significantly alter traders’ perceptions of supply risks.

Source: Get the Data

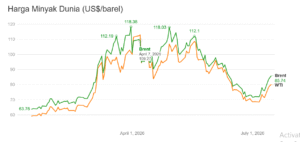

Source: Get the DataOil prices have surged significantly over the past few days. On Tuesday, July 14, 2026, Brent crude rose 1.72% to $84.73 per barrel, while WTI gained 1.5% to $79.34 per barrel, extending a two-day rally that has now exceeded 11%. The upward trend continued on Wednesday, with both benchmarks climbing further. What is particularly striking, however, is that the price surge is not being driven by an actual decline in production, rather by a rising risk premium stemming from the uncertainty surrounding shipping routes. Those concerns are not unfounded. The number of vessels transiting the Strait of Hormuz has fallen sharply compared to pre-conflict levels, as attacks on tankers have made shipping companies far more cautious.

Source: CNBC Indonesia

This comes despite the IEA’s July 2026 report showing a fairly strong production recovery in June, with global supply and gulf exports surging as previously delayed tankers finally started moving again. However, those figures remain well below pre-conflict levels, and most of the recovery has been concentrated in crude oil rather than refined products. Meanwhile, ongoing attacks on Russian refineries have further constrained global supplies of diesel and gasoline. On the demand side, the IEA expects consumption to begin recovering, although overall demand for 2026 is still projected to be lower than last year’s.

Forecasts from major financial institutions remain highly divergent. Goldman Sachs has adopted a more cautious stance, pointing to weakening demand from China and Europe as key downside risks that could push prices lower. Barclays, on the other hand, is sticking with its high-price outlook, arguing that the effective closure of the strait has already removed a significant portion of global supply from the market, while global inventories continue to decline. Citigroup has even raised its projections, warning of the possibility of extreme price spikes if disruptions in the strait persist. Meanwhile, BP reported a drop in quarterly production due to operational setbacks in the Middle East. (AJM/MFA)

You may also like

Di Balik Status Tersangka Mantan Jampidsus: Ketika Kredibilitas Kejaksaan Diuji

Rapat Tanpa Agenda di Kepala Sendiri

Pertahanan Kini Bukan Sekadar Soal Senjata: Perpres Baru Kategorikan Penyebaran Budaya LGBTQ sebagai Ancaman Nonmiliter

Di Balik Mimpi Besar dan Kota yang Makin Padat, Apakah Masih Worth It Merantau ke Jakarta?

Upaya Perdamaian Iran dan AS: Harapan Baru di Tengah Proses Diplomasi